Power Before Chips: How Behind-the-Meter Generation is Rewiring the AI Race

AI Workloads are battling an ageing power grid. Speed-to-power is the new currency.

Key Messages:

The US grid cannot keep pace with AI’s power demands — interconnection queues stretch 4–7 years, 70% of grid infrastructure is over 25 years old, and 600 GW of planned US data centre capacity is still searching for power.

Behind-the-meter generation is not a workaround — it is the new architecture — from trailer-mounted gas turbines and reciprocating engines to solid-oxide fuel cells and SMRs, BTM solutions are being deployed at gigawatt scale by hyperscalers today, with xAI, OpenAI, Oracle and others already committing billions.

Capital will follow power — the winners in the AI race will be those who solve the electron problem first; US policy, commercial models, and technology are all converging to make BTM the structural backbone of next-generation data centre infrastructure.

The collision between growing AI compute demand, and a slow-moving national electrical grid is now a structural issue in US power markets.

Microsoft’s Satya Nadella, in a November 2025 podcast, put the operating constraint plainly: “The biggest issue we’re having now isn’t chips. It’s power.”

The response is behind-the-meter (BTM) power generation, deployed at the data centre and predominantly owned and operated by third parties

BTM solutions are not a temporary solution. From modular gas turbines, to solid-oxide fuel cells, small modular nuclear reactors, and battery energy storage systems, each of these will play a unique but structural role in the US grid and electron value-chain.

Demand

US Demand for power is committed and growing

Based on North American Electric Reliability Corporation’s (NERC) latest Long-Term Reliability Assessment, summer peak demand across the US bulk power system is forecast to grow by ~200 GW over the next ten years, a 70% increase versus the equivalent forecast a year earlier. Winter peak demand is forecast to grow by ~250 GW, a 65% increase.

JLL's 2026 Global Data Center Outlook forecasts global data centre capacity nearly doubling from 100 GW to 200 GW by 2030, with the US accounting for roughly 60 GW or 60% of that increase.

The data centre pipeline is far larger. Roughly 600 GW of planned US DC capacity is currently searching for power, against 180 GW that has secured a utility supply agreement.

AI’s Unique Requirements

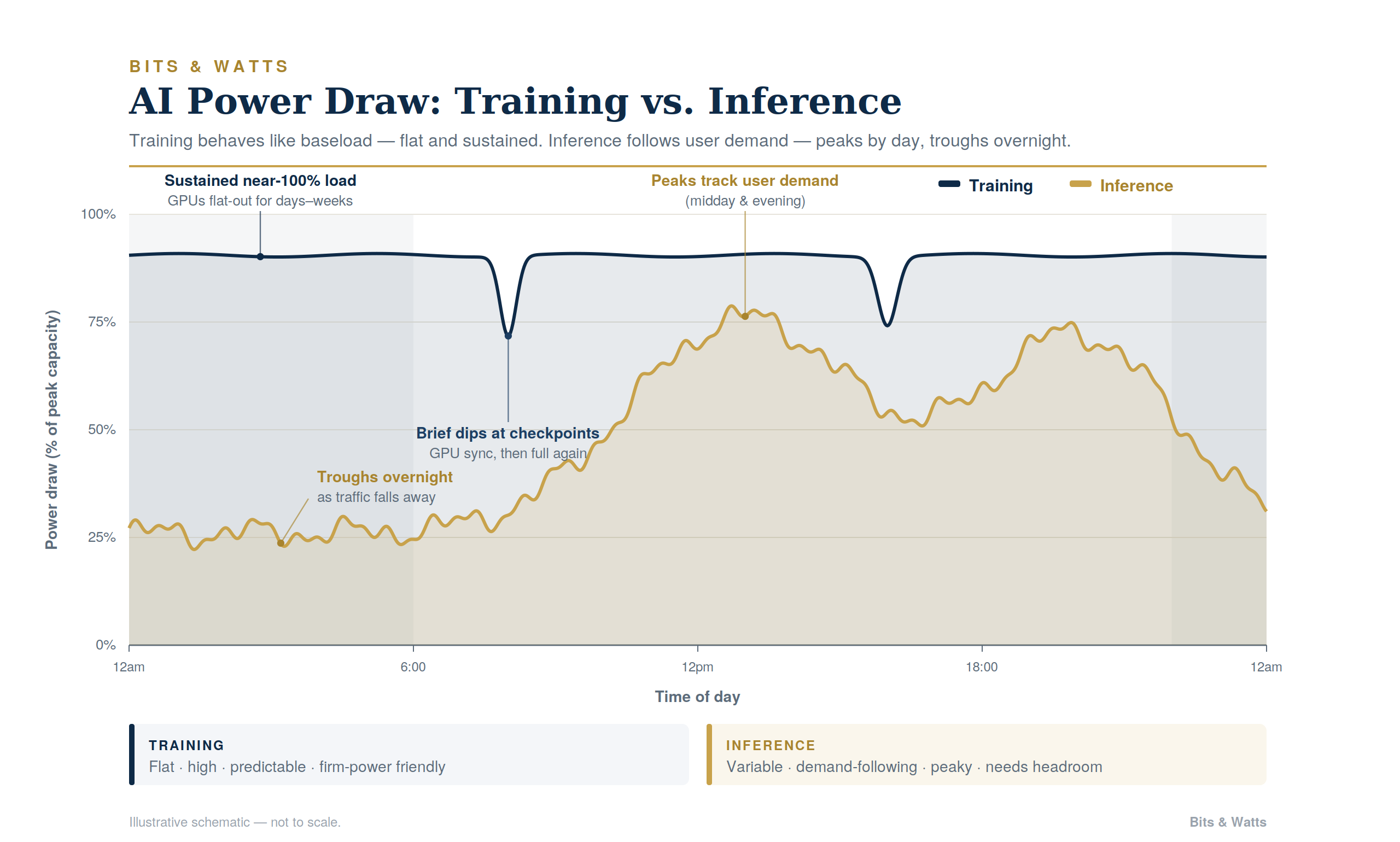

AI doesn’t simply add load. It also runs continuously, and concentrates at a density the grid was never built for.

AI Large Language Model (LLM) training is the compute-intensive process of building an AI model (e.g. Claude Opus, GPT, Gemini). This is done by feeding it vast datasets across hundreds of thousands of GPUs for week or months, to learn the statistical patterns of language.

Always-on inference. Inference is the user-facing layer: every query, every API call, every agent action, served at low latency, 24 hours a day. At Nvidia GTC 2026, Jensen Huang suggested that inference has overtaken LLM training as the dominant AI workload.

Power density requirement. Traditional data center racks drew ~12 kW. AI racks today draw 41–130 kW. Nvidia’s next-generation Vera Rubin and Kyber architectures are being designed around an 800V direct current rack delivering up to 1 MW per rack by 2027–2028. The 54V intermediate-voltage architecture that served data centers for over a decade cannot carry this density.

The AI-driven demand for power is structural. The question is whether supply can deliver.

Supply

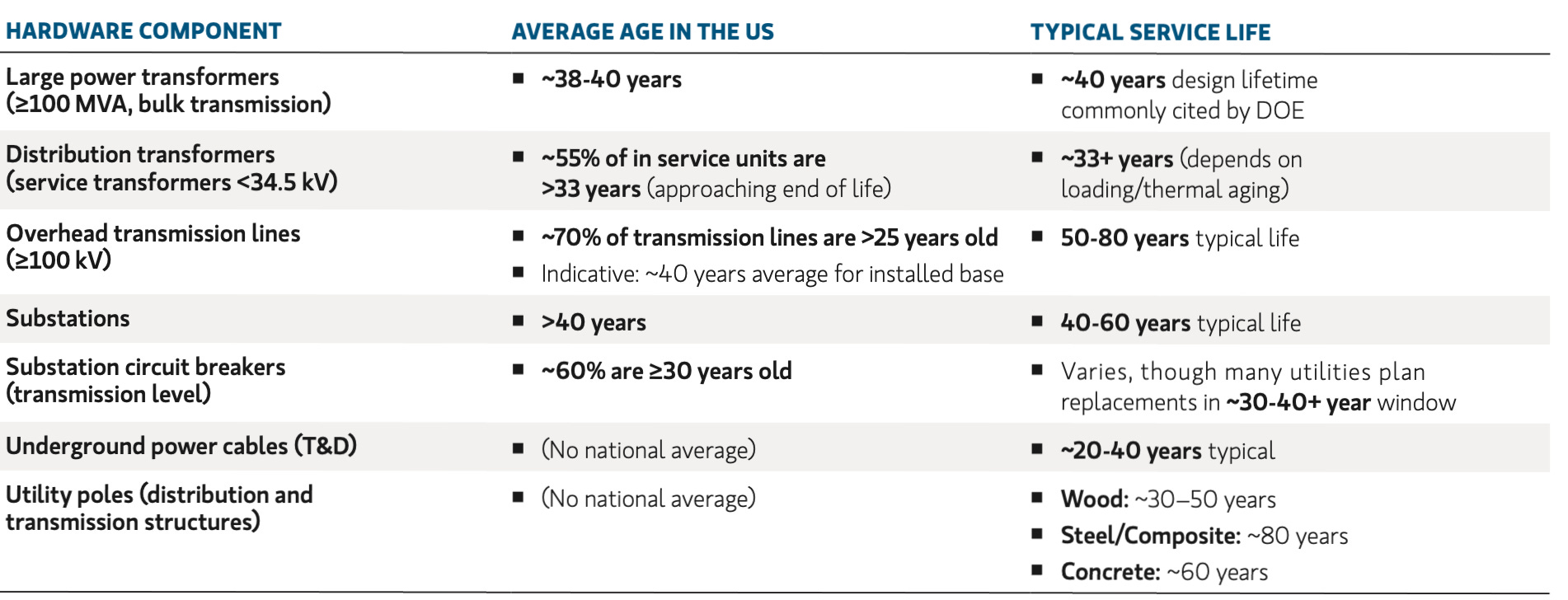

The US grid is not ready for AI workloads. Most of the bulk power system was constructed between the late 1950s and 1970s, sized for a fraction of today's electricity intensity.

Ageing Grid: According to the US Department of Energy, 70% of US power transformers and transmission lines are over 25 years old. 60% of circuit breakers are over 30. The American Society of Civil Engineers grades US energy infrastructure D+. Replacement lead times have stretched to 18–36 months, a binding constraint on every utility expansion plan.

The interconnection queue is the second supply-side constraint primarily driven by an overwhelming number of requests inclusive speculative ones, and the long lead-time required for engineering-studies to approve the requests. Average wait time for a power connection in the US has risen to four years, and in primary markets such as Northern Virginia, “quick power” is now defined as Q4 2027.

Ageing equipment and multi-year interconnection queues does not allow the US to “play to win”. Policy is the lever to relieve the supply constraint.

The geopolitical backdrop & policy response

In April 2026, Bessent put out an urgent message to the American public: “If China is the casino, artificial intelligence is the table stakes. If we don’t win in AI, then it’s game over.”

Nvidia CEO Jensen Huang has warned that China could overtake the US in AI precisely because its abundant energy lets it cluster large numbers of chips for compute power.

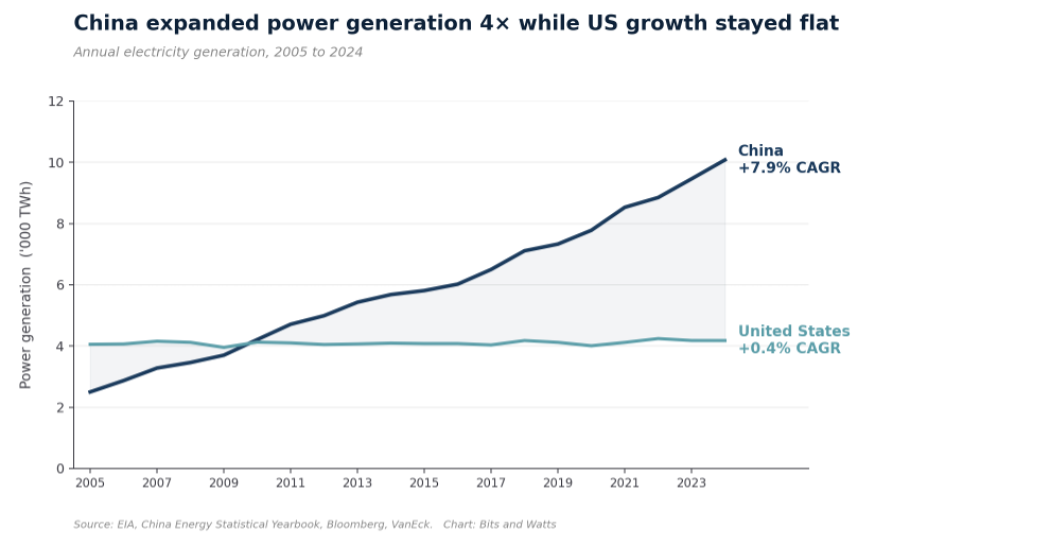

US vs China: The structural backdrop is a two-decade asymmetry. Since 2005, China has expanded power generation at ~8% CAGR; the US at 0.4%. China added roughly 540 GW of new capacity in 2025 alone, eight times US net additions that year.

AI Action Plan: The US Government has responded with an action plan - probably the most explicit federal endorsement of dispatchable generation since the late 1970s. On July 23, 2025, the White House released - Winning the Race: America's AI Action Plan. Pillar number 2 supporting this plan, titled ‘Build American AI Infrastructure’, outlines the policy actions required to Develop a Grid to Match the Pace of AI Innovation. This includes (1) Stabilising the grid (2) Optimising existing grid resources (3) Prioritising interconnection & exploring new energy sources.

Whilst the US government is pulling out all stops in the broader war of chip + energy supremacy, the journey to secure electrons has already begun - machines are being wheeled from oilfields to data centres and the ink is drying on behind-the-meter (BTM) power deals.

Why behind-the-meter matters

Before we dive into the various power solutions, we first need to understand what is Behind-the-meter (BTM) power and why it matters.

BTM is power generation deployed on the customer side of the utility meter, owned and operated as part of the data centre and it is distinct from the national power grid. BTM has been generally used as either ‘emergency power’ or ‘bridge power’ for data centres, oilfields, or other industrial facilities.

Today, BTM is a core element of next-generation data centre architecture with numerous benefits.

Time-to-power: With the grid interconnection wait times at 4-7 years, BTM enables time to power of ~6-18 months for data centres owners which reduces the opportunity cost for data center developers (e.g. Vantage) and hyperscalers (e.g. Nvidia). Every year of delayed deployment results in billions of lost revenue.

Reliability and Resilience: AI data centres are increasingly used for agentic AI workload which requires “always on inference” and/or LLM Training, requiring more power and uptime. On-site power generation with battery storages means improved reliability and resilience because the data centre is not reliant on the grid which can be an issue during peak grid demand and outages.

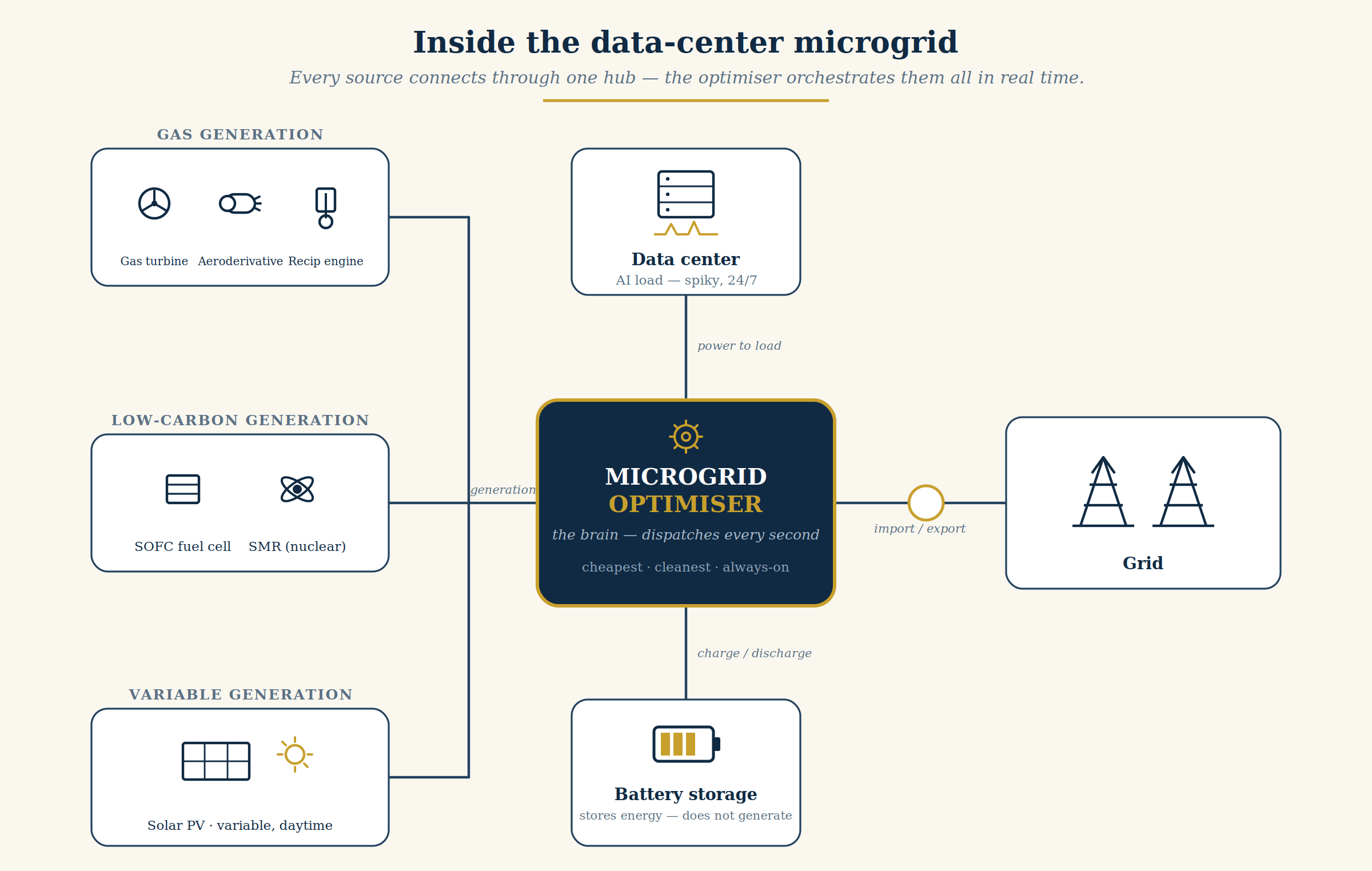

Optimisation: BTM solutions along with a microgrid optimisation software allows for the data center to pull power as required on-demand. It also gives it the flexibility to buy additional power from the grid or sell surplus power capacity back to the grid.

We now breakdown BTM solutions into 3 core pillars:

(1)Generation (2)Storage (3)Optimisation

BTM Generation

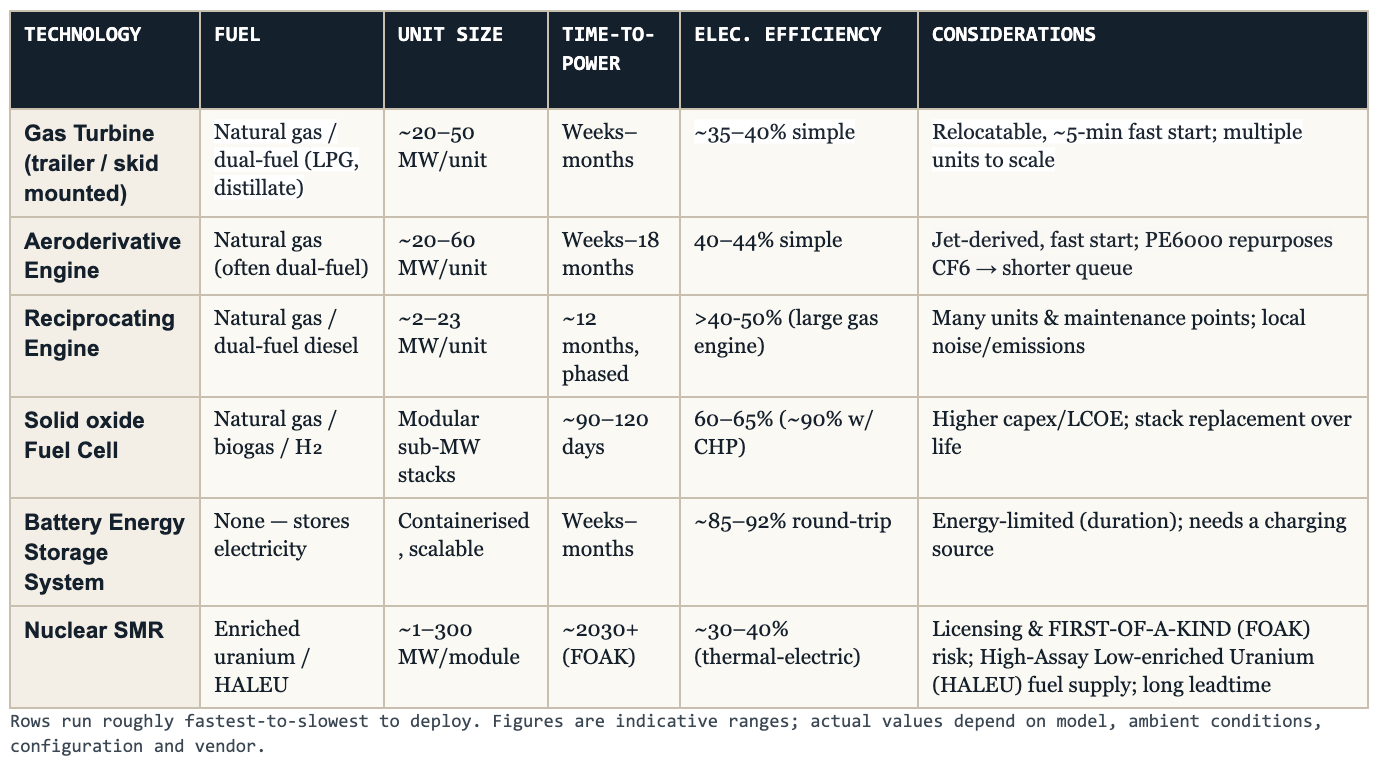

The BTM generation stack spans three broad solution sets, each with its own time-to-power and economic profile.

Combustion-based: Gas turbines, aeroderivatives and reciprocating engines are combustion machines, they burn fuel (natural gas, LPG, diesel, Kerosene, and alternative fuels including hydrogen blends) to spin a generator.

Gas Turbines

CCGT (Combined Cycle Gas turbines)

newly inaugurated 1,260-MW Dania Beach Clean Energy Center (DBEC) in Broward County on June 1, 2022. Courtesy: GE")

CCGTs pressurise incoming air, combusts it with fuel and the resulting hot and high-pressure gas expands through the turbine to spin a generator. Leftover heat generated is then recycled to generate steam. This second cycle of recycling exhaust heat makes it highly efficient at ~60%.

However, since backlogs range from 4-7 years, data center developers turn to alternatives such as industrial/mobile scale turbine generators which can be deployed faster, albeit less efficient.

Industrial (Trailer-mounted) Gas Turbines

This is the "bridge power" play for data centers waiting on grid interconnection: get megawatts on-site fast. Trailer-mounted turbines which run a simple-cycle (no steam recovery), generating 16-40MW of power, and can be deployed and operational in weeks rather than years. You sacrifice efficiency (~30-40%) for speed of deployment and flexibility — operators stack many units to scale up, then relocate them later.

Elon Musk disrupted the data center industry by deploying a 100k Nvidia GPU supercomputer (Colossus) in just 122 days, operational in July 2024. With the Memphis grid unable to meet power demand, xAI turned to Solaris Energy's Solar Titan mobile gas turbines and Voltagrid reciprocating engines — some still on-site as grid substations gradually come online. xAI has since acquired the former Duke Energy site, which is planned to host 40+ such turbines generating over 1GW to power Colossus 2 and 3.

Capex Committments: CTC Property (a subsidiary of xAI) has entered into a 49%-51% JV with Solaris Energy, with >US100million in capex already committed to building turbines. This is a clear signal of continued demand.

The xAI precedent will force hyperscalers to rethink their approach and timelines. Powering up the site at this speed using mobile gas turbines and acquiring land to build a self-supply power plant sets a new industry benchmark for the hyperscalers and showcases what ‘energy de-bottlenecking’ via BTM can achieve.

Aeroderivative (mobile) Gas Turbines

Derived from jet engines, they are lightweight, compactly mounted on a skid, easy to deploy on-site, and starts fast (~5 minutes from a cold start to peak power), with a lower emissions-footprint compared to larger industrial turbines. Because units are factory-built and even truck-mountable (GE’s LM2500, Mitsubishi’s FT8, Boom Superpower and similar), they are the go-to bridge power while a slower primary source or grid connection is built out.

OpenAI & Crusoe deployed GE Vernova’s LM2500 at Stargate Abilene, delivering about 1GW of power.

Crusoe has also ordered 29 Boom Supersonic units each rated at 42MW in a 40 feet shipping container sized package.

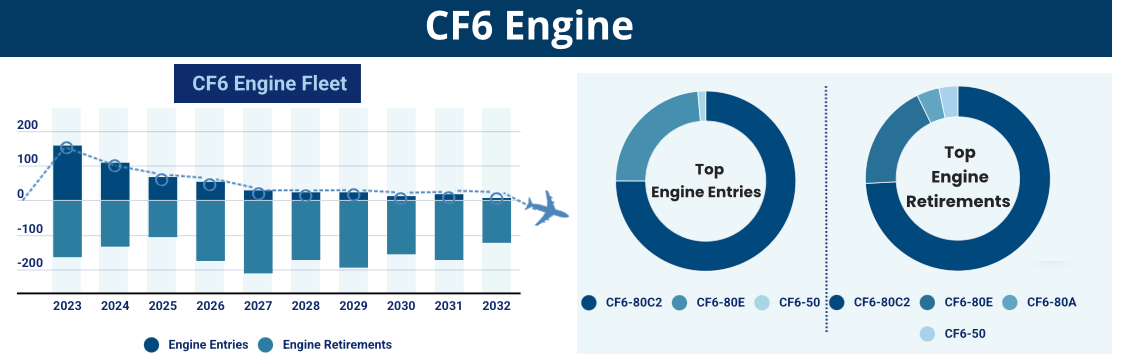

Jet Engine retirements present an opportune moment for the industry to repurpose them into mobile turbines for data centre use. CF6-80C2 jet engines (the current undisputed workhorse of the global air cargo fleet) will see a large retirement of more than 1000 engines over the next decade. Turbine manufacturers like GE Vernova & ProEnergy stand to benefit, with ProEnergy already set to deliver >20 turbines for deployment 2027 onwards. to repurpose them into mobile turbines for data centre use.

Other manufacturers including Mitsubishi, using Pratt & Whitney Engines, and Siemens, which acquired the Rolls Royce turbine business years ago, already provide industrial power and will likely grow their market share in the data centre segment in years to come.

Reciprocating Engines

These are large internal-combustion piston engines similar to locomotive engines driving a generator. Reciprocating engines (RECIs) start rapidly and reach full power within minutes. Each typically provides ~20mw of power, and, is able to respond to rapid load fluctuations.

VoltaGrid, a key player in this space, uses Jenbacher J624 & J620 engines, and modularises them via their proprietary “QPAC” system, to provide a robust BTM solution to Data Centers. VoltaGrid’s business model is power as a service (PaaS) which is essentially a subscription based model, not requiring any initial capex investment.

We note strong deployment and pipeline deals for RECIs -

xAI leveraged VoltaGrid as an initial power source when setting up Colossus, alongside the Industrial Turbine (Trailer mounted) by Solaris Energy.

Oracle & VoltaGrid agreed for supply up to 2.3GW for Stargate project.

Vantage Data Centers' Project Frontier, a $25B mega-campus in Texas, will host

VoltaGrid's first QPAC deployments with expected installed capacity of 2GW.

Liberty Energy will be supplying Vantage data center customers with Bergen Engines for a total capacity of 400MW in 2027, and up to 1GW thereafter.

Engine manufacturer order books are being filled on the back of firm demand from data centers -

VoltaGrid inked a deal with INNIO group in Feb 2026, for production of 300 x 25MW Jenbacher gas engines, with delivery scheduled by 2028.

Liberty has signed an agreement with Bergen in May 2026, to supply up to 45 x 11MW generator sets, amounting to a total capacity of ~500MW for Data Centers across USA.

Solid-oxide fuel cells (SOFC)

Fuel cells are differentiated by the type of electrolyte utilised. The most mature and commercially viable ones are polymer electrolyte membrane (PEM) and solid-oxide (SOFC). PEM is being developed and used in automobile industry - case in point is Hyundai & Kia’s partnership with Gore. It has not scaled up in production as rapidly as SOFC has in recent years and is more expensive due to use of materials like platinum as a catalyst. Here, we focus on SOFCs.

A solid oxide fuel cell (SOFC) generates electricity from fuel without combustion. Natural gas is reformed internally into a hydrogen-rich stream, and at roughly 700–900°C oxygen ions migrate across a ceramic electrolyte to react with that fuel, pushing electrons through an external circuit as direct current (DC).

Solid Oxide Fuel cells are clean and scalable: No combustion of fuel and no flame means negligible harmful gaseous emissions like NOₓ or SOₓ, less use of water, and low noise pollution.

Units are modular “copy-and-paste” stacks that scale incrementally — and ship fast. Goldman Sachs estimates fuel cells could supply 25%-50% of total behind-the-meter power demand by 2030.

Notably, because the output is already Direct Current (DC), SOFCs are a natural fit for next-generation 800V DC data centers, where the power ultimately consumed by the chips is DC anyway.

This is the technology that gained traction in 2025–26:

Bloom Energy is set to supply data centres and utility players, with multi-gigawatt deals in the pipeline:

Oracle/Project Jupiter up to 2.5 GW - Oracle shifted away from an initial plan to use turbines and adopted Bloom’s SOFC instead, proving that fuel cells can provide a firm baseload and not just peaking or backup power.

Brookfield committed to invest $5B to deploy Boom’s SOFC in their data center sites.

American Electric Power (AEP), one of the largest utility players in USA, signed a supply agreement for up to 1GW of Boom SOFC.

Ceres Power is another player in SOFC, with a different technology and commercial approach to Bloom. Ceres uses a 3rd generation metal supported fuel cell technology, which they have pioneered. Using a steel metal substrate to support a thinner electrolyte layer, it can operate at a significantly lower temperature of ~450-630°C. Ceres partners the likes of Doosan, to manufacture their power system which claims to have 65% electrical efficiency and a 5% per second power ramp rate, as well as being more structurally robust. While Bloom has the first-mover advantage in USA, using a tried and tested approach, Ceres’ 3rd gen technology is currently focused for deployment in UK/Europe and production in Korea/China.

Small modular nuclear reactor (SMR)

SMRs are nuclear fission reactors shrunk to a fraction of a conventional nuclear plant size and fabricated in a factory, to be then shipped in standardised modules for assembly on site. They are deemed to be safer, due to passive safety systems which ensure the reactor uses basic laws of physics to be self-stabilising and cooled naturally.

On 23 May 2025, President Trump signed four executive orders to launch an American nuclear renaissance. The executive orders laid out plans to (1) modernize nuclear regulation, (2) streamline nuclear reactor testing, (3) deploy nuclear reactors for national security, and (4) reinvigorate the nuclear industrial base.

In January 2026, the Department of Energy (DOE) committed US$2.7 billion to build a domestic supply chain for the two fuels these reactors run on: low-enriched uranium (LEU) and high-assay low-enriched uranium (HALEU). Both increase uranium’s active component (U-235), with LEU enriched to 3–5% and HALEU to roughly 15%. Higher enrichment packs more energy into less volume, allowing longer operating cycles, smaller cores, and reduce waste, which is why about two-thirds of SMR designs are built around HALEU.

Together, these policies and initiatives lay a strong foundation and springboard for the development of SMRs — which are first-of-its-kind advanced reactors that have quicker development cycles compared to 10-15 years required to build a conventional nuclear power plant.

To date, there are more than 80 SMR designs at various development stages with 3 players worth spotlighting.

Oklo (a company previously chaired by Sam Altman) signed a deal with Meta to develop 1.2GW nuclear power campus consisting of Oklo’s Aurora SMRs to power Meta’s data centers in Ohio with first phase targetted 2030 and 1.2GW expected by 2034. While this is a front of meter solution in the PJM interconnection grid, it is likely that Meta has a conditional offtake with Oklo, ensuring optionality for both parties and the possibility for households to also enjoy added capacity in the grid.

X-energy signed a deal with Amazon to deploy 5GW of SMRs in the US by 2039.

NuScale: One of America’s largest (on paper) SMR deployment plan (6GW) is claimed by NuScale’s partnership with Entra1 Energy & Tennessee Valley Authority (TVA), though details on deployment and deals with hyperscalers are absent at the moment.

Testing, manufacturing, and deployment all take time, so meaningful capacity only arrives and ramps from 2030 onward. Meanwhile, regulatory tailwinds prevail with latest announcement in May 2026, outlining $94 million in grants to American companies to expedite deployment of SMRs.

Storage

Battery energy storage systems (BESS) are containerised banks of batteries, mostly lithium-ion, that sit between a power source and the data center ‘load’, charging when power is in surplus and discharging when it is needed.

Keeping up with AI power spikes: As explained in the earlier section ‘Why BTM Matters’, AI-Training runs synchronize 100,000s of GPUs, resulting in load swings between idle and full power in sub-seconds. Pulling energy required for those spikes strains the grid, causing voltage instability.

A battery system on-site is the solution, as it absorbs the power swings, discharging itself to cover each spike and recharging during the lull.

The battery storage space is highly competitive with Chinese (e.g. Sungrow, CATL) & Korean (LG Energy, Samsung SDI) value chain players. American companies are trying to make headway with Fluence, Tesla and Crusoe+Redwood being notable players in the market.

Fluence Energy: Fluence provides a complete package to customers - storage, along with software optimisation and other services. Its flagship Smartstack system delivers 7.5MWh per unit with Smart Control and monitoring systems embedded within. In June 2026, Fluence joined Siemens and Nvidia on the DSX Vera Rubin AI-factory reference design. Fluence’s Smartstack is incorporated into the design, as handling voltage/frequency instabilities, demand response and AI load smoothing. Fluence’s success rests on whether it signs hyperscaler deals in Q3/Q4 2026.

Tesla Megapacks: This is a vertically integrated utility-scale solution with the same hardware (Lithium batteries packed in containerised modules) assembled in the US. ~USD 400 million worth of megapacks are expected to be installed at xAI’s Colossus II.

Crusoe + Redwood Materials: This falls into a unique “circular-economy” category of the BESS theme. These 2 pioneers commissioned the largest solar + second-life battery microgrid in North America. Totalling 12MWh of solar capacity paired with 63MWh of storage built entirely from repurposed EV batteries, this solar + storage grid powers Crusoe’s Spark data centers in Nevada/ This is a proof of concept that solar plus storage can possibly sidestep multi-year interconnection queues, and confidently carry AI load.

How do the various BTM Solutions Stack Up?

Optimisation

AI data centre wired to multiple BTM generation sources and the national grid, is just raw power. What turns it into a ‘microgrid’ is the optimiser software which sits in the middle, making quick sub-second decisions on where the next watt should come from, ensuring the data center stays up through outages.

This matters because AI clusters don’t draw power smoothly. Tens of thousands of GPUs ramp in sync, so load spikes and collapses second-by-second, far faster than a turbine’s shaft can respond. The battery sits in between charging on dips, discharging on spikes so generators see steady demand and GPUs get the power they require.

All monitored and controlled by the microgrid’s command centre.

The Journey Ahead

The journey ahead for the “bits” will be determined by the “watts”.

Jensen Huang has warned us “Every data centre of the future will be power-limited”.

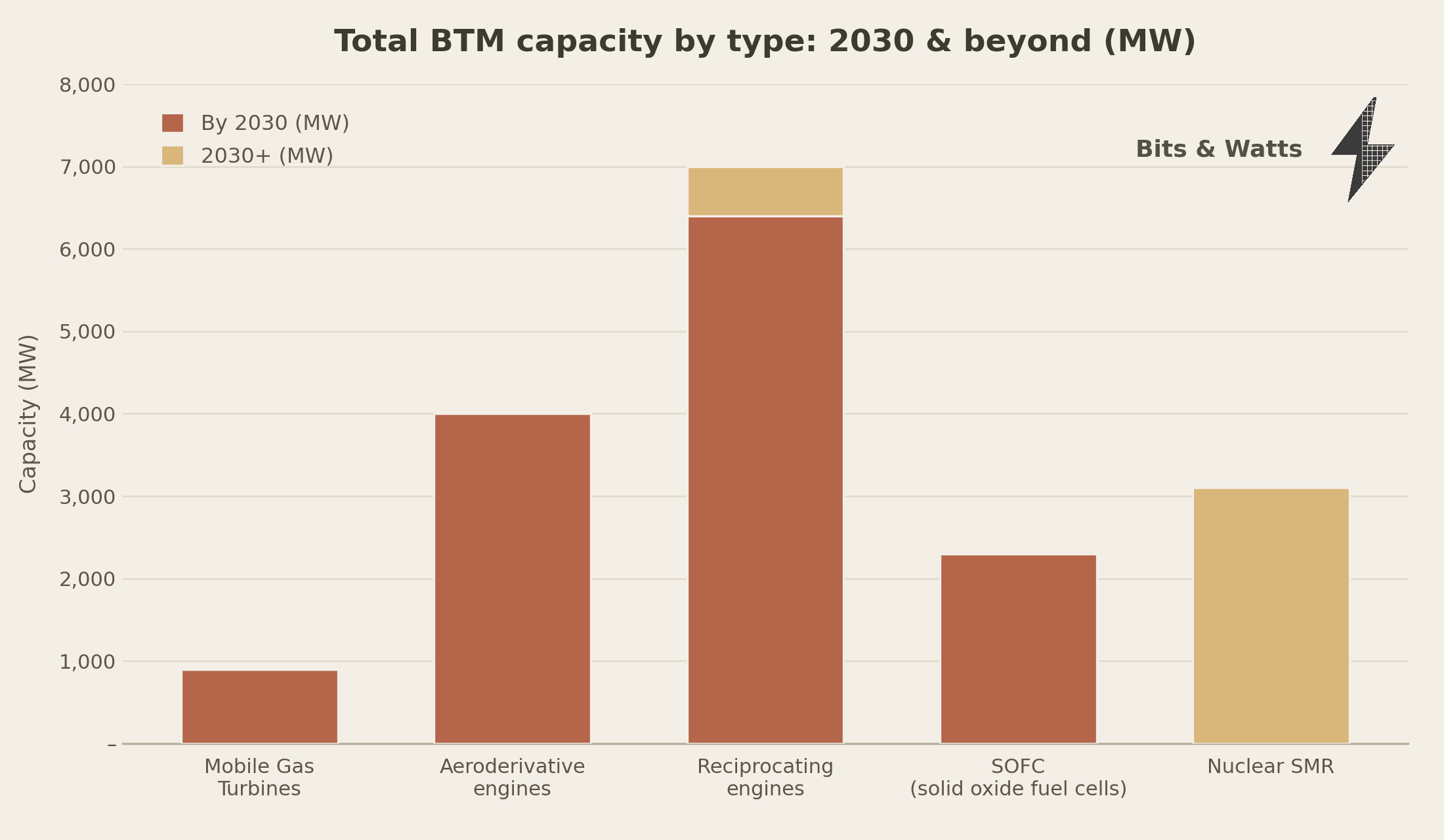

As of Mid June 2026, approximately 14GW is committed for deployment by 2030. 14GW of BTM capacity accounts for one-quarter of expected data center power growth between now and 2030.

Gas solutions are leading the race to 2030: Gas-driven turbines & engines capture ~80% of market share while SOFC holds ~20%. this is mostly driven by the availability of gas turbines and engines with SOFC still in production, testing & early deployment stage with firm deals.

Post 2030 we expect SMR to catch up: While details of post 2030 deployment are scant, we expect that SOFC is likely to gain additional market share as it is seen as a longer-term solution for a firm baseload given its high efficiency & low polluting concerns. Nuclear SMR will kick-in mostly post-2030 - however how SMR demand will pick up is a matter of early deployment risk & competition with traditional nuclear plants.

Pulling multiple levers to de-bottleneck power is table stakes. There will be no one size fits all - a confluence of factors ranging from state policy, to availability of natural resources such as gas, will determine the suite of generation solutions deployed on site. Elon Musk set a precedent with xAI, building a site at the border of 2 states to navigate state policies, combining multiple BTM solutions including trailer-mounted turbines, reciprocating engines, and battery storage, at various stages of the data centre set up, along with real estate acquisition required to physically house the required generation equipment.

We expect US AI Action Plan to catalyse the alignment of state and federal policies. While the federal government sees data centre expansion as a national security interest, states often remain restrictive when permitting, due to water use limits and grid cost-sharing mandates for e.g. Hyperscalers will need to navigate this highly fragmented market. States are under pressure to re-align policies and make exemptions, as they compete to attract new investment and collectively help the USA fight in the race to AI-dominance.

Commercial models will evolve, as equipment manufacturers like INNIO and data centre real estate providers like Vantage, may look to differentiate themselves and offer guaranteed power as a key value proposition to attract hyperscalers. Crusoe is a fine example - purpose-built data centres with BTM generation, thereby offering hyperscalers a viable operational solution from the outset. Supply from the grid will coexist with BTM in the long run, as existing utility providers with diversified energy mix (e.g. Constellation Energy, Vistra, NextEra and TVA) catch-up to provide affordable & stable supply.

Nuclear generation through SMRs could be a game changer, because it is viewed from a national security lens, it increases the grid capacity and is also highly sustainable. A clear signpost will be additional SMR-power deals signed with hyperscalers in Q3 / Q4 2026. Although data centres will be the catalyst for SMRs to come online, SMRs may stand to benefit more from being front of the meter, as it adds sustainable capacity into the national grid, allowing the likes of Oklo to possibly benefit from state and federal policy and also de-risks data center demand dependency.

Eventually, capital will follow power!

In our next post, we deep dive into the world of fission and the global nuclear renaissance.

| A guest post by

|

| A guest post by

|

| A guest post by

|